De-dollarization 2009-2019

Process to change the system, de-dollarization 2009 – 2019.

Although the International Monetary Fund (IMF) has served as the world’s principal forum for the promotion of international monetary cooperation and maintains an essential tool kit for this purpose (SDR and affiliated Funds), the Fund has not been fully able to cope with the deficiencies of the present dollar-based system.

In the context of recent worldwide finance crisis in autumn 2009, the UNCTAD issued a report calling for a new reserve currency based on the SDR, managed by a new global reserve bank. The report called for abandoning the US dollar as the single major reserve currency and stated that the new reserve system should not be based on a single currency or even multiple national currencies but instead permit the emission of international liquidity to create a more stable global financial system. The IMF released a report in February 2011, stating that using SDRs could help stabilize the global financial system. These institutionalized efforts have not been particular attractive to create any viable new system substituting the US dollar system.

After the world financial crisis of 2008-2010, the process of de-dollarization began in the world economy. Increasingly more countries around the world, especially in Asia, are striving to decrease their use of American currency in their foreign trade. Doing so helps them to protect their financial systems from risks associated with fluctuations in the dollar’s rate and to strengthen their own currencies. De-dollarization simplifies financial operations by reducing the number of transaction steps and helping to save time and money. De-dollarization also has political significance.

De-dollarization process, run by China, Russia and Iran

At the forefront of the world de-dollarization process are America’s main economic competitors and political rivals: China, Russia and Iran. Moscow is dropping the US dollar in major arms deals and switching to the Russian ruble and the national currencies of its partners. The euro is currently an alternative to the dollar, with US currency used only when there is no other way. Russia has signed the supply contracts on the air defense systems with India, Turkey and China. The agreement with India implies the settlement of the trade in rubles. In doing so, India avoided the risk of having transactions blocked by US authorities.

In August 2017, the United States passed a new law, the Countering America’s Adversaries Through Sanctions Act (CAATSA). The law allows also for secondary sanctions to be imposed against states and organizations working with countries that the US considers “enemies”. According to the law, the US may freeze their dollar accounts and transfers made outside American jurisdiction. American companies are also prohibited from working with countries and organizations listed in deals with US enemies. In September 2018, China found itself under secondary sanctions for purchasing Russian S-400 missile systems. A host of high-ranking Chinese individuals and organizations involved in the defense purchase for China’s armed forces had their access to dollar operations blocked.

Russia and China have been working intensely to switch to payments in national currencies, since 2015. Most experts believe that the switch to national currencies in Russia’s economic relations with China and India could change the world finance scene. The decision to eschew the US dollar by three powerful and wealthy countries could lead to a notable drop in the dollar’s exchange rate and with time to the end of its primary position in the world economy.

While the role of oil-producing countries (and particularly Saudi Arabia) should not be underestimated, at present the driving forces with regard to de-dollarization are primarily Moscow and Beijing. There exist numerous political statements in this context which leave no room for doubt. The Russians and Chinese are quite open about their views regarding the role of gold in the current phase of the transition. The gradual move away from the US dollar to a multipolar monetary order has several important effects, which only make sense when viewed through this lens.

Position of EU and Europe in the process

In January 2018, many central banks in Europe revealed plans to hold yuan as part of their foreign currency reserves, highlighting the Chinese currency’s rise into an elite league of the world’s major reserve currencies. The role of the yuan has increased steadily since the International Monetary Fund included the currency in its Special Drawing Right basket from October 2016, placing it into an elite group that includes the euro, the dollar, the Japanese yen and the British pound.

The European Union is considering switching payments from the US dollar to the euro after Washington threatened to target with sanctions on European firms working in Iran, according to European reports, in May 2018. In August 2018, German foreign minister Heiko Maas called for the creation of a new SWIFT-payments system independent of the United States and EU’s Juncker strongly underlined the need to use euro instead of dollar in September.

In mid-November, 2018, French President Emmanuel Macron admitted in an exclusive interview with CNN that the European nations have so far failed to provide a viable alternative to the US dollar and have become excessively dependent on the American currency. The French president stated that “This is an issue of sovereignty for me. So that’s why I want us to work very closely with our financial institutions, at the European levels and with all the partners, in order to build a capacity to be less dependent from the dollar.”

On September 12, 2018, Jean-Claude Juncker, European Commission President, is throwing down the gauntlet. Juncker is not a nationalist populist but he devoted his State of the European Union address to the defense of “European sovereignty.” This means, among other things, using the euro to challenge the US dollar’s global dominance, particularly in an era of growing American unilateralism. “The euro must become the face and the instrument of a new, more sovereign Europe,” Juncker said. “It is absurd that Europe pays for 80 percent of its energy import bill — worth 300 billion euro a year — in US dollar when only roughly 2 percent of our energy imports come from the United States. It is absurd that European companies buy European planes in dollars instead of euro.”

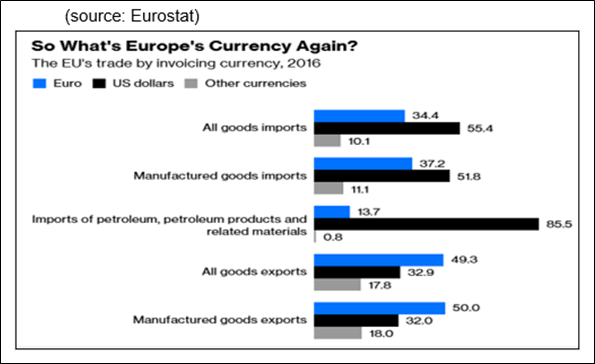

Juncker’s complaints about the dollar-denominated contracts are justified. For example, the EU is the biggest importer of crude oil. Yet, according to Eurostat, a vast majority of these imports is invoiced in US dollars. Moreover, half of Europe’s exports are sold in dollars rather than euros. This makes little sense, given that the euro is the world’s second-biggest reserve currency and, unlike the dollar, its share of global foreign exchange holdings is growing. In December 2018 the Commission presents actions to strengthen the role of the euro in a changing world. Promoting the euro’s international role is part of Europe’s commitment to an open, multilateral and rules-based global economy and trade. The Commission also calls on Member States to promote the wider use of the euro in strategic sectors.

“Prophetical forecast” of Storfele

Ronald-Peter Stoferle, a managing partner at the Liechtenstein-based investment fund Incrementum AG wrote on the website of Austrian based Mises Institute in September 2018 on this matter and later gave an interview to Switzerland’s Neue Zurcher Zeitung in mid-September 2018.

He seems to agree that the world is in the middle of a move away from a dollar-centric approach to world trade to a multipolar and multicurrency system. He explained that while the petrodollar system of world trade enabled the US to pursue an egoistic economic policy and accumulate a massive pile of debt, the creeping move away from the dollar, led by Russia and China, threatens to end this state of affairs.

Stoferle explains that during a changeover from one global currency to another, the gold (and to a lesser extent silver) has always played a decisive role. Central banks and governments have long been aware that the dollar has a sell-by date as a reserve currency. But it has taken until now for the subject to be discussed openly.

Most mainstream economists avoid the topic like the plague. The issue is too politically charged. However, that does not make it any less important for investors to look for answers, on the contrary. The following questions need to be asked:

What indications are there that the world is turning its back on the US dollar? What are the clues that gold’s role could be strengthened in a new system?

Stoferle finalizes his statement by saying “the process of moving away from the dollar, prepared by Europe and triggered by China and Russia, can no longer be stopped and as a “supra-national” reserve asset, gold plays an important role in it.”

Position of Saudi Arabia

For a long time, the basis on which this global currency system rests, was poorly documented. Finally, Bloomberg published a comprehensive article in May 2016, which provided detailed confirmation of the agreement that was hitherto only known as a rumor.

The fact that this article is published now also represents a subtle clue that there are simmering shifts in the global currency system. As stated before, this article confirmed the fact that the US and Saudi Arabia made an agreement of “petrodollar” and “recycling of it”.

The world is looking for alternatives to the dollar and finds them more and more often. The trend becomes ever more tangible and can be described by the term: de-dollarization. A clear signal that something is afoot would be the abolition of the Saudi riyal’s peg to the US dollar.

As recently as April 2018, Saudi Arabian economist Nasser Saeedi advised Middle Eastern countries to prepare for a “new normal” and specifically to review the dollar pegs of their currencies: “By 2025 it is clear that the center of global economic geography is very much in Asia. What we’ve been living in over the past two decades is a very big shift in the political, economic, and financial geography.”

The summary list of major countries pursuing de-dollarization

Global tensions caused by economic sanctions and trade conflicts triggered by Washington, have forced targeted countries to take a fresh look at alternative payment systems currently dominated by the US dollar. Here below is the list of major de-dollarization countries taken steps towards eliminating their reliance on the US dollar and the reasons behind their decisions.

China

The ongoing trade conflict between the US and China as well as sanctions against Beijing’s biggest trading partners have forced China to take steps towards relieving the dollar dependence of the world’s second-largest economy. The Chinese government has not made any loud announcements on the issue. However, the People’s Bank of China has been regularly reducing the country’s share of US Treasuries, being still number-two foreign holder of the US sovereign debt.

Moreover, instead of promptly dumping the dollar, China is trying to internationalize its own currency, the yuan, which was included in the IMF basket alongside the US dollar, the Japanese yen, the euro, and the British pound. Beijing has recently made several steps towards strengthening the yuan, including accumulating gold reserves, launching yuan-priced crude oil futures and using the currency in trade with international partners.

As part of its Belt and Road Initiative, China is planning to introduce swap facilities in participating countries to promote the use of the yuan. Moreover, the country is actively pushing for a free-trade agreement called the Regional Comprehensive Economic Partnership (RCEP), which will include the countries of Southeast Asia. RCEP includes 16 country signatories and the potential pact is expected to form a union of nearly 3.4 billion people based on a combined $49.5 trillion economy, which accounts for nearly 40 percent of the world’s GDP.

India

Ranked the world’s sixth-largest economy, India is one of the biggest merchandise importers. It is not surprising that the country is directly affected by most global geopolitical conflicts and is significantly impacted by sanctions applied to its trading partners.

Delhi switched to ruble payments on supplies of Russian S-400 air-defense systems as a result of US economic penalties introduced against Moscow. The country had to switch to the rupee in purchases of Iranian crude after Washington reinstituted sanctions against Tehran. In December 2018, India and the United Arab Emirates sealed a currency-swap agreement to boost trade and investment without the involvement of a third currency. Taking into account that India is the third-largest country by purchasing power parity, steps of this kind could considerably diminish the role of the dollar in global trading.

Turkey

Earlier in 2018, Turkish President Recep Tayyip Erdogan announced plans to end the US dollar monopoly via a new policy that is aimed at non-dollar trading with the country’s international partners. Later, Turkey’s leader announced that Ankara is preparing to conduct trade through national currencies with China, Russia and Ukraine. Turkey also discussed a possible replacement of the US dollar with national currencies in trade transactions with Iran.

The move was prompted by political and economic reasons. Relations between Ankara and Washington have been deteriorating since the failed military coup in the country to oust President Erdogan in 2016. It is been reported that Erdogan suspects US involvement in the uprising. The Turkish economy sank after Washington introduced economic sanctions over the arrest of US evangelical pastor Andrew Brunson on terrorism charges in relation to the uprising. Erdogan has repeatedly slammed Washington for unleashing a global trade war, sanctioning Turkey and trying to isolate Iran. The NATO member’s decision to buy Russian S-400 missile systems added fuel to the fire. Moreover, Turkey is trying to ditch the dollar in an attempt to support its national currency.

Iran

A return of Iran to the global trading arena did not last long. Shortly after winning the US presidential election, Donald Trump opted to withdraw from the 2015 nuclear deal (JCPOA) signed between Tehran and a group of nations, including the UK, US, France, Germany, Russia, China, and the EU.

The oil-rich nation has once again become a target for severe sanctions resumed by Washington, which has also threatened to introduce penalties against any countries that would violate the embargo. The punitive measures banned business deals with the Islamic Republic and cracked down on the country’s oil industry. Sanctions have forced Tehran to look for alternatives to the US dollar as payment for its oil exports. Iran agreed a deal for oil settlements with India using the Indian rupee. It also negotiated a barter deal with neighboring Iraq. The partners are also planning to use the Iraqi dinar for mutual transactions to reduce reliance on the US dollar amid banking problems connected to US sanctions.

Switzerland and Iran have developed a payment channel to bypass US sanctions, launched in January 2019. A special financial mechanism aimed at maintaining trade ties between Switzerland and Iran is ready for implementation. The Iran-Switzerland payment channel is designed to bypass US sanctions. The Swiss clearing house will be used to facilitate Iran’s oil transactions with its major Asian crude customers – namely India, China and South Korea. The two parties are preparing an independent payment channel in addition to the Special Purpose Vehicle (SPV). European Union is also working on a financial mechanism to ease non-dollar trade with Iran and circumvent US sanctions. It hopes the Swiss SPV will keep the nuclear deal alive.

Russia

President Vladimir Putin said the US is “making a colossal strategic mistake” by “undermining confidence in the dollar.” Russian Finance Minister Siluanov said earlier in 2018 that the country had to dump its holdings of US Treasuries in favor of more secure assets, such as the ruble, the euro, and precious metals.

The country has already taken several steps towards de-dollarizing the economy due to the constantly growing burden of sanctions that have been introduced since 2014 over a number of issues. Russia has developed a national payment system as an alternative to SWIFT, Visa and Mastercard after the US threatened tougher new sanctions that would target Russia’s financial system. So far, Moscow has managed to partially phase out the greenback from its exports, signing currency-swap agreements with a number of countries including China, India and Iran. Russia has recently proposed using the euro instead of the US dollar in trade with the European Union. Once a top-10 holder of US sovereign debt, Russia has all but eliminated its holdings of US Treasuries. Moscow has used the money to boost the nation’s foreign reserves and to build up its gold stockpile to stabilize the ruble.

The future of the dollar and its role in financial diplomacy

Still a dollar

The dollar’s central role in world financial markets has reflected both faith in American leadership and the absence of reasonable alternatives. Currency dominance has been a linchpin in America’s efforts to shape a global order around free Western markets and Western democracy while serving as a foundation for the sustained growth of a more integrated global economy.

This role now faces rising risks. One sign is the weakening faith in America’s ability to hold the system together. The clues are in the early elements of financial arrangements that bypass dollar markets, international financial institutions without active US participation and increasing economic gatherings of finance ministers.

The global trade, production and consumption arena has become a three-way race among Asia, Europe and the US but the international currency system has long been and still is dominated by the US dollar, highlighting a mismatch between the real global economy and international currency system. This mismatch has turned out to be the major contradiction facing the global economy and financial system, fueling the China-US trade dispute and prompting reforms in the global economic governance system.

Potential alternatives

The global economy and the trade governance system have shifted from an old model in which other economies were orbiting around the US toward a three-horse race (the US, EU and China) meaning that de-dollarization is inevitable.

Europe’s common currency, euro was a political project to bind the continent after centuries of war, although a clear aspiration of some European leaders has been to create a counterweight to dollar dominance. Yet the European financial crisis fragmented its financial markets and triggered questions about the viability of the European project itself.

Postwar Japan deliberately protected the yen from an international role so that domestic capital could be directed for domestic purposes and the exchange rate could be managed. More recently, Japanese economic woes and competition from China have proscribed any real role for the yen, which remains at roughly 4.5 percent of international reserves.

Chinese officials have a clear aim to expand the role of the renminbi in global trade, finance and sovereign reserves. For example, foreign governments have issued debt and central banks have established swap lines in Chinese currency. Even the likes of Germany and Chile have added it to the mix of their global reserves. Yet for now the reach of China’s currency remains restricted. Chinese yuan gains international popularity amid accelerated BRI cooperation

Chinese currency renminbi (RMB), or the yuan, has gained a bigger popularity overseas, especially in countries along the BRI process and international demand for RMB is increasing.

“Final word”

Currency power ultimately depends on trust in the intentions of the issuer. The issuer’s interests may naturally come first but its usage will grow if these interests are essentially aligned with shared goals of global growth and stability. The US and its military and political allies have had difficult negotiation processes for decades to create present monetary and financial policies and institutions. The ability to impose order on global markets is, in many ways, what distinguishes the dollar from other international currencies.

In the same ways that the overwhelming power of the US military has been able to force order onto a conflict zone, so the US Federal Reserve and Treasury have played pivotal roles in stabilizing financial markets through swap lines and loans. Pressures on the dollar’s role have been rising gradually abroad. Doubts about US financial leadership deepened sharply during a global financial crisis 2008 that was triggered by what many considered American carelessness that allowed worthless subprime real estate assets to infect the world’s financial system.