Economic capability of Russia

Economic outlook and debt position of Russia

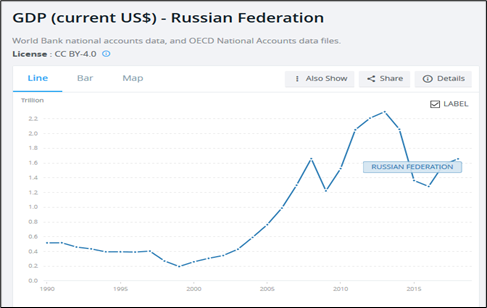

Russia’s economic downfall is clearly observable after the collapse of Soviet Union reaching the bottom in late Yeltsin’s years of 90s. A new upswing, from the beginning of the new millennium, lasted nearly ten years ending to the worldwide finance crisis 2009. Some years of moderate growth followed the new period of different sanctions and other punitive measures, imposed by the US and other Western countries. Russia has faced an economic Roller Coaster for the period after the Cold War.

Western analysts have frequently criticized that the lack of structural economic reforms is the crucial factor behind the low growth in the Russian economy. However, a large number of important measures have been made by the Russian Government during the last few years.

The main reasons for “Roller Coaster” of Russian national economy are oil price fluctuations, foreign sanctions and domestic, “ultra-tight” and cautious finance and monetary policy focusing mainly on protective measures against foreign punitive actions.

Here below a list of ten major structural reforms during last few years, aimed for the long term strengthening of economic base of Russian society.

1. Phasing out of oil export tax

In June 2018, Russian government announced that it is phasing out the oil export tax. The Russian energy and finance ministries agreed with oil companies to start cutting the export duty on crude gradually, to bring it from the current 30 percent to zero over the next six years (up to 2024). The duty will be cut by 5 percent annually over the period, as part of a wider tax reform that seeks to replace the export duties and mineral resources extraction taxes with a single tax based on the profits that oil companies in Russia make.

2. The VAT rate increase from 18% to 20%

December 29, 2018, the value-added tax (VAT) rate in Russia will amount to 20% starting from January 1, 2019. Russian President Vladimir Putin signed a law in the autumn of 2018, stipulating an increase of the VAT rate from 18% to 20%, as well as new tariffs for social contributions. According to the Russian Finance Ministry’s calculations, the move will boost budget revenues by 620 bln rubles ($8.9 bln) per annum. Legal entities pay the value-added tax in Russia at all stages of production and sale of goods or services.

3. Growing forex reserves, low debt and high reserves

Gold’s share is on steady rise in Russia’s financial reserves, when Russia’s gold purchases have been at record high, Russia being the biggest monetary gold purchaser in last five years in the world. The share of monetary gold in Russian international reserves as of the year end 2018 reached to 2.112,0 tons, making Russia as the fifth biggest monetary gold holder in the world. There has been a strong shift from US dollars to euros, yuans and yens in the assortment of foreign currencies held by Russian Central Bank. Russia liquidates nearly all its holdings of US debt and invests money in gold. Total amount of forex reserves exceeded $ 550 billion in late autumn 2019.

Despite facing years of sanctions from the US and EU, the Russian economy is growing again. Russia’s foreign debt stands at $454 billion at the end of 2018 (GDP-ratio under 15%), making Russia one of the lowest debt-ratio states in the world. According to The Central Bank of Russia (CBR) report the total amount of Russia’s external debt is now at the lowest level in nearly 10 years. A balanced budget is another reason why Russia does not need to borrow abroad. In the year 2018 Russia will have a budget surplus – the first in seven years with the Finance Ministry expecting state revenues to exceed outlays by more than half a trillion rubles ($16 billion).

Foreign debt may become a major problem if market conditions suddenly change for the worse. Therefore, CBR has kept the principle “The smaller the debt, the lesser the chances of a default.” The key basic rationale behind “the policy of the low debt and high buffer reserves & just moderate economic growth” is the deliberate and willful endeavour to teflonize the Russian national economy against outside sanctions and other punitive measures. The strategy is designed to avoid a repeat of 2014 when the West imposed sanctions on Moscow and the rouble to plunge.

4. Official de-dollarization plan of the Russian economy, 2018 – 2024

In September 2018, Russia’s VTB Bank President Andrey Kostin unveiled his four-part plan to abandon the US dollar in Russia’s transactions with foreign states. The head of the Russian Lower House Committee for Financial Markets, MP Anatoly Aksakov, backed a plan to completely stop using the US dollar, noting that the program can be completed in three to five years. Aksakov believes that Western nations will not lift the sanctions against Russia any time soon but instead will likely impose new, even harsher restrictions.

Russian Finance Minister Anton Siluanov said in October 2018, that the plan on de-dollarization of the Russian economy had already been prepared and submitted to the government. According to the plan, Russia seeks to fully de-dollarize the economy by 2024.

The program is long and complicated but its key point is that Russian exporters who use rubles instead of dollars would get huge taxation benefits including quicker VAT returns and other stimulus to ditch the greenback. It is also necessary to gradually switch to such a system of international payments, which implies payment in rubles for Russia’s goods on the world market like oil, gas and arms exclusively. Russia should also unite with China and the European Union in creating a payment system that cannot be controlled by the United States (the alternative to the SWIFT).

5. National development project for Russian economy, in late 2018

The savings strategy of Russian Government is fiscally ultra-cautious and prudent and will come at the expense of economic growth. Russia’s drive to fill state coffers to give itself buffer against threats like new US sanctions makes sense but will come at the expense of economic growth. President Putin expects that the government can support the economic growth rate above 3% after 2021. Putin believes that changes in the country’s economic structure, innovations, commitment to implementation of national projects will trigger GDP growth rates. Russian government is going to allocate over $300 billion in coming years for domestic development covering 12 national development projects.

6. Russian Pension Reform, 2018

The plan of the Russian pension reform was unexpectedly announced by the Government of Russia on June 14, 2018.The decision was followed a series of countrywide protest actions and demonstrations in the Russian Federation, with the major requirements of abandoning the planned retirement age hike. The reform of Russia’s pension system has undoubtedly become the country’s main economic news of the year 2018. Under the new plan, to be implemented from 2019, the retirement age for men will be increased gradually from 60 to 65. President Putin has softened planned pension changes following angry protests and a slump in his approval rating. He said the retirement age for women would be increased from 55 to 60 instead of to 63 but a five-year increase for men, to 65, would stay. Women with three or more children could retire earlier.

7. Russian pivot to East

President Putin’s May 2012 Edicts are an obligatory reference, when marking the inception of a new approach to the development and growth of Russian economy. Putin’s executive order covers measures to implement foreign policy moving away from the West to the East. The 2008–2009 worldwide finance and economic crisis was a cold shower for Russia. Not only the seven percent annual growth from 2000 to mid-2008 that was hoped to bring about the doubling of the economy in ten years was interrupted but subsequent developments proved that it could hardly be restored unless fundamental changes capable of upgrading and diversifying the economic structure intervened.

Russia’s economic interest in China increased substantially after the economic breakdown caused by the 2008 crisis and the successive collapse of commodity and energy prices. From 2008 on China was evolving to the first trade partner for Russia replacing Germany. Slow and uncertain recovery after the crisis increased the perception of economic fragility among policy makers. The Russian major policy rethinking, forced by events, made Russia’s turn eastwards gaining steam.

Since September 2015, Vladivostok in Russian Far East, has hosted the Eastern Economic Forum (EEF), the showcase for Russia’s “turn to the East policy”. Russia’s leadership describes the economic and political pivot to Asia as the country’s foreign policy priority in the 21st century. Russian President Putin made his first-ever state visit to Singapore in November 2018, coinciding with the 33rd ASEAN summit, 3rd ASEAN–Russia summit, 13th East Asia Summit (EAS), and 50th anniversary of diplomatic relations between Russia and Singapore. In addition to China, Russia has large and growing trade relations among others with India, Japan, South Korea and Vietnam, EAEU being a special cooperation organization.

8. Russia’s agriculture and food business

Russian exports of agricultural products and foodstuffs have grown 16-fold since 2000. In 2016, Russia became the world leader in wheat exports. Since the early 2000s, the country’s share of the world wheat market has quadrupled, from four to 16 percent. Food is today Russia’s second biggest export sector after oil and gas, helping to diversify the economy away from energy. In 2017, the volume of exports of Russian food products and agricultural raw materials amounted to $20.7 billion.

9. Capital outflows and repatriation

The illegal exodus of capital has been one of the biggest problems for the Russian economy since the collapse of the Soviet Union. Looking over Russia’s capital flight data, it is easy to see the biggest development problem of Russia’s economy: the oligarchs make their profits in Russia but take the money abroad. Moscow has not released a definitive figure for the amount of wealth held by Russians overseas. However, the National Bureau of Economic Research estimates the value at 75 percent of Russia’s national income or about one trillion US dollars. Since 1994, when the Central Bank of Russia (CBR) started publishing capital flight data, a total of $581bn has left Russia as private sector outflows. This sum could have been spent on the country’s economy but is now moved abroad for other purposes. Capital flight has diminished off in the last two years, but some $20billion is still leaving every year. Russian Governmenthas offered various ways for the money to be returned to Russia, including the amnesty of capital and Eurobonds with preferable tax regime. The returned money can become an alternative financing instrument for the state if new US sanctions prohibit foreign investors from buying sovereign bonds of Russia.

10. Russia’s digital economy and AI

According to World Bank Report (General assessment of Russia, by World Bank Group 2018) Russia has made significant strides in its digital transformation process. In spring 2018, 73% of Russian households enjoy broadband internet access, with active mobile broadband penetration at 75%. Russia has the highest number of fibre connections in Europe and over 60% of the population now owns smartphones. The number of users of online government and municipal services has doubled in just one year to reach 40 million. Over the last six years, ICT exports have more than doubled, reaching over $ 8.5 billion in 2017, while several Russian ICT companies have emerged as global players like Yandex and Kaspersky Lab. The gains in usage of emerging technologies are especially rapid in data analytics, cloud computing, the Internet of Things, 3D printing, robotics, artificial intelligence and blockchain-technology.

As digitization remains a top priority at the highest level of government, Russia is driving digital transformation across the Eurasian space, leading digital initiatives at the international, national, regional and local levels. The Russia Digital Economy Program adopted in July 2017, the EAEU Digital Agenda passed in 2017, and a variety of digital initiatives at the regional/oblast level are all elements in this vision.

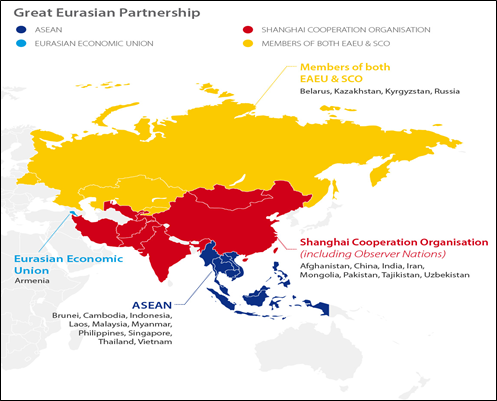

Eurasian Theater, Greater Eurasian Partnership and BRI

Two great initiatives, Great Eurasian Partnership pursued by Russia and BRI pursued by China are “walking hand in hand” in Central Asian Region, covering step-by-step more countries and regions and including more economic and political activities. Eurasian integration outlook is tightening now after the US withdrawal from JCPOA.

Iran’s top trading partner is China, while Tehran and Moscow have been improving ties as the three countries move closer to cementing a solid “practical alliance”. From Beijing’s view, Iran is absolutely a key hub of BRI, where the 926 km high-speed railway from Tehran to China is a key BRI project. Chinese companies are developing oil refineries, massive oil and natural gas fields in Iran.

Russia has made large volume trades with Iran in aviation, both civil and military, as well as in energy business. Both Iran and Russia are fighting US sanctions. Despite historical frictions, Iran and Russia are getting closer in their business and political relations. Tehran provides crucial strategic depth to Moscow’s Southwest Asia presence and Moscow unequivocally supports the JCPOA. Iran will become a formal member of the Russia-led Eurasia Economic Union (EAEU) before the end of 2019 and with solid Russian backing, Iran is accepted as a full member of the Shanghai Cooperation Organization (SCO) by 2019.

A priority area for Russia–China cooperation is the development of the Eurasian region within the framework of the Belt and Road Initiative and the Greater Eurasian Partnership. The pairing of the Chinese Belt and Road Initiative (BRI) and Russia’s supported Eurasian Economic Union (EAEU) in recent years has turned into an important part of the whole complex of Russia-China interaction.

In May 2018, China and the Russia-led EAEU signed an agreement on trade and economic cooperation, the first major systematic arrangement ever reached between the two sides. The China-Russia plans may go still further. Both Chinese President Xi Jinping and Russian President Vladimir Putin have openly discussed the possibility of uniting Eurasia and developing something wholly new entity, known as the Great Eurasian Partnership. This concept brings together the members of the Eurasian Economic Union (EAEU), Shanghai Cooperation Organization (SCO), and ASEAN as a huge free trade bloc.

Although it will take decades to achieve, such initiatives do mean that China and Russia are going to be collaborating on trade, economy, security and overall development in deeper and more complex ways in the coming years and decades. Russia will be China’s trade corridor to and from Europe as well as a trade, cargo and transportation facilitator between the two, not to mention the multi-aspect security issues.